January 27, 2023

2023 Outlook - Emerging Markets

The worries and concerns that kept investors away from emerging markets (EM) for more than 18 months are slowly dissipating. In 2022, accelerating inflation and tighter U.S. financial conditions – as reflected by increasing U.S. rates, higher credit spreads and a strong U.S. dollar - weighted on emerging market equities (see graph 1). However, in 2023 most of these headwinds are expected to be replaced by declining inflation (especially goods inflation), peaking in rates and a stable to somewhat-weaker U.S. dollar. Within emerging markets, the re-opening of China and the subsequent economic recovery should also herald the end of an 18-month decline in China’s economic growth.

Sources: MSCI Inc., Bloomberg Finance L.P., The Goldman Sachs Group, Inc., as of December 19, 2022

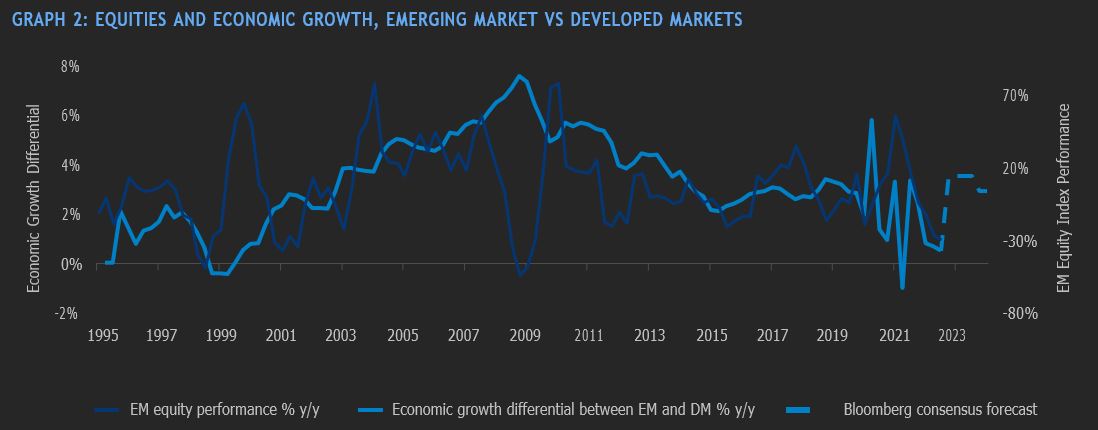

After two years of underperformance, emerging market equities are set to outperform their developed market peers in 2023, partly driven by the increasing economic growth differential widening once again in favour of emerging markets (graph 2).

Sources: Bloomberg Finance L.P., MSCI Inc., as of September 30, 2022

CHINA

Health concerns (zero-Covid policy), political changes (following the 20th Party Congress) and a struggling economy (property, debt and regulations) had pushed equity valuations down to multi-decade lows by the end of October 2022, retesting the lows recorded in March 2020. However, cautious expectations of China moving to a more flexible Covid policy by March 2023 was brought forward after a wave of protests in China. Both the timing (ahead of the winter season and Chinese New Year) and the pace of the re- opening caught investors by surprise. Although the subsequent increase in case counts and hospitalization rates will make for a bumpy reopening early in 2023, our base case remains that the reopening process will continue and gain further momentum during first half of 2023 and that the economic benefits of the reopening will become more evident from Q2 onwards.

Our conviction in a strong economic recovery in China in 2023 is further affirmed by several fiscal support measures that the government had announced late in 2022 to benefit households, SMEs, innovation and the struggling real estate market. The opening up of the economy will benefit many sectors, but significant beneficiaries would be the property market, consumer spending and the service sector. China’s economic cycle stands out amongst the major economies with meaningfully higher expected growth in 2023 than 2022.

REST OF EMERGING ASIA

A large part of emerging Asia (excluding China) is driven by tech-heavy Taiwan and South Korea. Though we remain constructive on the semiconductor and memory sectors over the long run, near-term dynamics of weaker demand could weigh on these sectors well into 2023. India remains an outlier in terms of (expensive) valuation and we take a more cautious approach despite strong fundamentals.

LATIN AMERICA

Many Latin American central banks are quickly approaching the end of their tightening cycles and, following hikes from 2% to 13.75%, the Brazilian central bank announced a pause in the hiking cycle in October 2022. However, the region tends to be more cyclical and closely tied to the global economic cycle. Expectations of a recession in Europe and the U.S. in 2023 leaves us more cautious when it comes to investments in the region. In addition, local politics, especially in Brazil and Peru, further complicate the investment outlook for the region.

VALUATION

Although technical factors by and in themselves are not compelling reasons to make a longer-term investment decision, they serve as trend enhancers or inhibitors. Valuation, both in historical and relative terms, as well as light positioning by global investors, argue well for emerging market equities when economic growth returns to Asia in a more meaningful way. Our base case is for “when” and not “if” growth returns in 2023, although a deep and prolonged global recession would challenge our 2023 view.

GLOSSARY OF TERMS:

Correlation: A statistical measure of how two securities move in relation to one another. Positive correlation indicates similar movements, up or down, while negative correlation indicates opposite movements (when one rises, the other falls).

Credit rating/risk – An assessment of the creditworthiness of a borrower in general terms or with respect to a particular debt or financial obligation. Credit risk is the risk of default on a debt that may arise from a borrower failing to make required payment.

Drawdown: Measures the peak-to-trough decline of an investment or, in other words, the difference between the highest and lowest price over a given timeframe.

Duration – A measure of the sensitivity of the price of a fixed income investment to a change in interest rates. Duration is expressed as number of years. The price of a bond with a longer duration would be expected to rise (fall) more than the price of a bond with lower duration when interest rates fall (rise).

Leverage – An investment strategy of using borrowed money – specifically, the use of various financial instruments or borrowed capital – to increase the potential return of an investment.

Return (absolute) – The measure of what an investment returned over a given time period. An investment that rose from $1,000 to $1,100 would have an absolute return of 10%.

Return (relative) – The performance of one investment versus another. The most commonly reported relative returns are mutual fund returns relative to their benchmark indexes.

Volatility – Measures how much the price of a security, derivative or index fluctuates. The most commonly used measure of volatility when it comes to investment funds is standard deviation.

Yield Curve - A line that plots the interest rates of bonds having equal credit quality but differing maturity dates. A normal or steep yield curve indicates that long-term interest rates are higher than short-term interest rates. A flat yield curve indicates that short-term rates are in line with long-term rates, whereas an inverted yield curve indicates that short-term rates are higher than long-term rates.

About the Author

Matthew Strauss has more than 25 years of global investment experience. Mr. Strauss joined CI in 2011 to help manage currency overlays and oversee the emerging market equity mandates. He is currently the lead manager on CI Global Select Equity fund and co-manager of the CI Global Income and Growth mandate. He also serves on the Asset Allocation Committee. As lead portfolio manager for the global and emerging market equity mandates, Matthew provides macroeconomic, country and sector strategies for these mandates. He has extensive international experience, having worked as Chief Strategist at the largest retail bank in Africa and as Senior Fixed Income and Currency Strategist at RBC Capital Markets. Matthew holds the Chartered Financial Analyst designation, a Bachelor of Commerce degree and an MA in Economics from the University of Stellenbosch, South Africa.

IMPORTANT DISCLAIMERS

This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication.Market conditions may change which may impact the information contained in this document. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies.

The opinions expressed in the communication are solely those of the authors and are not to be used or construed as investment advice or as an endorsement or recommendation of any entity or security discussed.

Certain statements in this document are forwardlooking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” or “estimate,” or other similar expressions.

Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what CI Global Asset Management and the portfolio manager believe to be reasonable assumptions, neither CI Global Asset Management nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.

The author and/or a member of their immediate family may hold specific holdings/securities discussed in this document. Any opinion or information provided are solely those of the author and does not constitute investment advice or an endorsement or recommendation of any entity or security discussed or provided by CI Global Asset Management.

Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document.

©CI Investments Inc. 2023. All rights reserved. Published January 4, 2023

About Us

Contact

- 15 York Street, 2nd floor

Toronto, ON M5J 0A3 - Phone: 416‑364‑1145 or

Toll-free: 1‑800‑268‑9374